There is no time to waste after getting in a motor vehicle accident. Though police officers and paramedics may handle vital steps needed to file a personal injury claim, there is still much for you to do to remain eligible for compensation.

Understanding the car insurance questions to ask after an accident can help you navigate the aftermath with less stress and more confidence.

Partnering with experienced Connecticut car accident lawyers can also significantly ease the process, helping you overcome common challenges and maximize your chances of securing fair compensation.

What To Know Before Asking Auto Insurance Questions

Every state has its own process for handling motor vehicle accidents. In states such as Connecticut, an at-fault system determines who could be financially responsible for accident injuries when your insurance can't or won't cover the damages you've sustained.

Connecticut requires drivers to carry minimum amounts of insurance coverage, which includes bodily injury liability and property damage liability.

However, these policies may be far from sufficient in covering the catastrophic injuries and extensive losses sustained in serious crashes such as rollover accidents or high-speed rear-end collisions. Moreover, obtaining compensation up to policy limits is a complicated process in itself.

As such, knowing what questions to ask and understanding the importance of seeking experienced legal help can prove invaluable in pursuing compensation.

How Long Do You Have To Call Your Insurance Company After An Accident?

It isn't uncommon for anyone in a car accident to have hesitation about contacting an insurance company. The stress of the collision itself and the confusion surrounding insurance policies often leave drivers wondering how long they have to get in touch with their insurer.

The general rule of thumb is to do so immediately after the accident, ideally within 30 days of the crash. Taking any longer could make the claims process more difficult.

If accident injuries make it challenging to complete daily tasks, let alone take on the bureaucratic complexities of an accident claim, consider hiring a lawyer as soon as possible to help with the process.

Regardless of when you call the insurance company or if a lawyer is helping you pursue a personal injury claim against the at-fault driver's policy, there are a few things you'll want to have ready before getting answers to car insurance questions:

- Your name as it appears on the policy

- Your policy number

- Identifying information for your vehicle, including year, make, and model; license plate number; VIN.

- The last four digits of your Social Security number and/or a personal identification number issued by the insurer

- A copy of the police report, if available

- Details about the accident, such as time, date, and location; names of other parties involved; nature of damages or injuries sustained

- Any photos or videos taken at the scene of the accident

- Contact information for any witnesses

- Medical records and bills related to injuries from the accident, if available

With this information readily available, claimants can ensure they provide accurate and thorough details when speaking with an insurance company or a lawyer. This may also help speed up the claims process and increase the chances of receiving fair compensation for damages sustained in the crash.

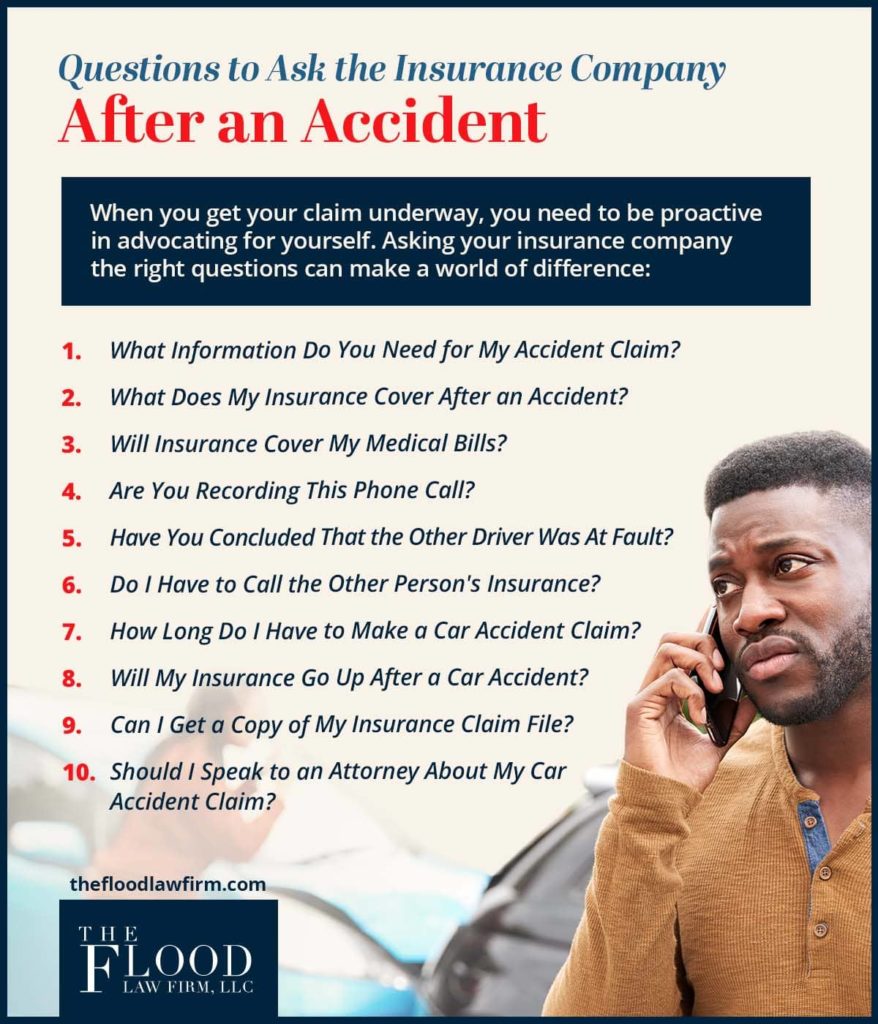

10 Questions To Ask Your Insurance Company After A Car Crash

1. Does my policy include coverage for this type of accident?

This question can set the foundation for the rest of the conversation. For Connecticut drivers with the minimum auto insurance policy, it is likely that you only have liability coverage for bodily injury and property damage.

This means that you may be covered for up to $25,000 per person for bodily injury and up to $50,000 per accident if multiple people are injured. For property damage, you may have up to $25,000 in coverage.

Insurance policies are thick with legal language and fine print, so understanding all the details can be challenging. This is where the assistance of a personal injury accident lawyer can prove invaluable.

Their understanding of insurance policies and experience in handling similar cases can help clarify your coverage and explore potential compensation options.

2. How long do I have to file an accident claim?

The time you have to file a claim may differ from the statute of limitations for filing a personal injury lawsuit. You may not be able to file one without the other. As such, you'll want confirmation from your insurer about filing deadlines that keep you on track to secure compensation for the damages and losses you have suffered.

If you're finding it challenging to get clear answers from your insurer, a lawyer can assist in navigating the complex legalities and deadlines associated with personal injury claims.

While the statute of limitations in Connecticut is two years, some circumstances, such as those involving government entities or minors, may have different deadlines. An experienced lawyer can assist in keeping track of critical deadlines to help avoid potential issues.

3. What are my financial responsibilities?

It's important to know what you may be responsible for financially after an accident. Your insurance policy may have deductibles you must pay out-of-pocket before your coverage kicks in. Additionally, the auto insurance company may not cover certain damages or losses.

Understanding your financial responsibilities can help you plan and budget for any potential expenses related to the accident. It can also help you understand what type of claim a lawyer can help you file against the at-fault party to recover compensation not offered by your insurance policy.

4. What damages will my policy cover?

Injuries from a car accident can cost several hundred thousand or millions of dollars over a lifetime. You want to make sure that you aren't stuck paying up-front or out-of-pocket costs that you might not be reimbursed for later. Find out as much as you can about what your policy covers, including medical expenses, lost wages, and pain and suffering.

If your insurer tells you something isn't covered, don't panic. This is another benefit of hiring an injury lawyer to help with your case. Their assistance may include negotiations aimed at achieving a better settlement from the insurer.

They can also help you file a personal injury claim or car accident lawsuit against the at-fault driver to seek compensation for injuries not covered by your policy.

By clarifying what may be included in your policy, you can better understand the right legal options for securing maximum compensation when someone else's negligent or intentional actions cause harm.

5. Have you concluded that the other driver is at fault?

Understanding who is at-fault can help when filing a car accident claim. If you believe the other driver was responsible, but your insurer disagrees, this could result in a denied claim or reduced compensation.

By asking this question, you can ensure that your insurer has accurately assessed the situation and determined liability correctly. If there is disagreement, it may be time to seek legal representation to fight for your rights and hold the responsible party accountable.

6. What documentation do you need to process my claim?

Coming prepared to the call with information such as the other driver's name, contact information, insurance details, and a police report may help speed up the claims process. However, your insurance company may require additional documentation, such as medical records or witness statements.

Sometimes, these items aren't available immediately. This is especially the case for medical records. It can take time for a medical professional to diagnose the full extent of injuries for the purpose of recovering compensation.

Fortunately, if you asked about how long it takes to file a claim earlier in the conversation, you'll understand how much time you have to gather these and other pertinent documents for submission to your insurer.

If you can't gather these documents on your own, it may be worth asking your personal injury attorney for assistance. They can help you collect and organize the necessary documents to support your claim.

7. Do I have to call the other driver's insurance company?

At this point in the conversation, you should have a better idea of what filing a claim with your insurer may look like. If your insurer isn't providing you the compensation you deserve or denies your claim unfairly, it may be time to contact the other driver's insurance company.

While this may seem daunting, having a personal injury attorney by your side can make the process easier. They can negotiate on your behalf and handle all communication with the other driver's insurance company. This allows you to focus on recovering from your injuries while knowing your legal rights are protected.

Those who try to handle this process independently often encounter obstacles such as low-ball settlement offers, pushback on liability, or delays in processing the claim. An experienced attorney can help combat these challenges to help you recover full and fair compensation from all available sources.

8. Will my auto insurance rates go up?

After filing a personal injury claim, one common concern is whether your insurance rates will increase. In most cases, your rates should not go up if you were not at fault for the accident.

However, it is possible that your rates increase if you are found partially responsible for the accident or have a history of getting into collisions. A lawyer can work to minimize your level of fault, potentially mitigating any increase in auto insurance premiums.

9. Are you recording this call?

After a car accident, asking if your call is being recorded is more than a formality—it's essential for protecting your claim.

Insurance companies such as State Farm, Allstate, and Geico often record calls under the guise of "quality assurance." However, these recordings may serve to minimize payouts or deny your claim altogether. A seemingly harmless statement could be taken out of context and used against you.

Many states require consent to record calls. However, provisions exist in Connecticut privacy statutes that allow insurers to circumvent direct consent by either announcing that calls will be recorded at the beginning of the call or playing a tone every 15 seconds that automatically serves as a form of consent.

If you are worried about your statements being taken out of context or used against you, consult with or hire a personal injury attorney before proceeding. They can either handle communications with the insurance company on your behalf or provide helpful tips for protecting your claim during recorded calls.

10. Can you send me a copy of my insurance claim filing?

By law, insurers must provide a copy of your claim filing upon request. This is important for several reasons:

- Reviewing the details: Sometimes, in the aftermath of an accident, it can be hard to remember all the details and information provided during the initial call. A copy of your insurance claim filing can help you ensure everything has been accurately documented.

- Checking for errors: Mistakes happen, especially when it comes to paperwork. By reviewing your claim filing, you can check for any errors or discrepancies that need to be corrected.

- Keeping records: Keeping records of important documents related to your personal injury claim is always a good idea. This includes written correspondence from your insurer, medical bills, and evidence that supports the claim.

This copy can also help your lawyer understand what has been included in your initial claim. Should any discrepancies arise, your lawyer can collaborate with you to address and correct them, strengthening your claim.

The Flood Law Firm | Personal Injury Lawyers That Can Help You File An Insurance Claim

You may or may not get the answers you want when you call your insurance company after a car accident. However, with the help of experienced personal injury attorneys from The Flood Law Firm, you can work towards recovering the compensation you deserve.

Our team is dedicated to fighting for the rights of accident victims and helping them navigate the complex process of filing an insurance claim or personal injury lawsuit.

Schedule a free case evaluation online or at (860) 346-2695 to learn what you should ask your insurance company after an accident, understand the legal options available based on their answers, and get guidance on protecting your right to compensation.